There has been a lot of discussion on the news lately regarding the Silicon Valley Bank in California failing. How did this happen? Where did the money go? I thought this would be a great day for us to have a conversation about banking, and how banking works. To make it as simplistic as possible, I found a comic book that I ordered several decades ago from the Federal Reserve Bank of New York. It tells a story of how money works, and I’m focusing on one particular section that discusses “Reserve Requirements”.

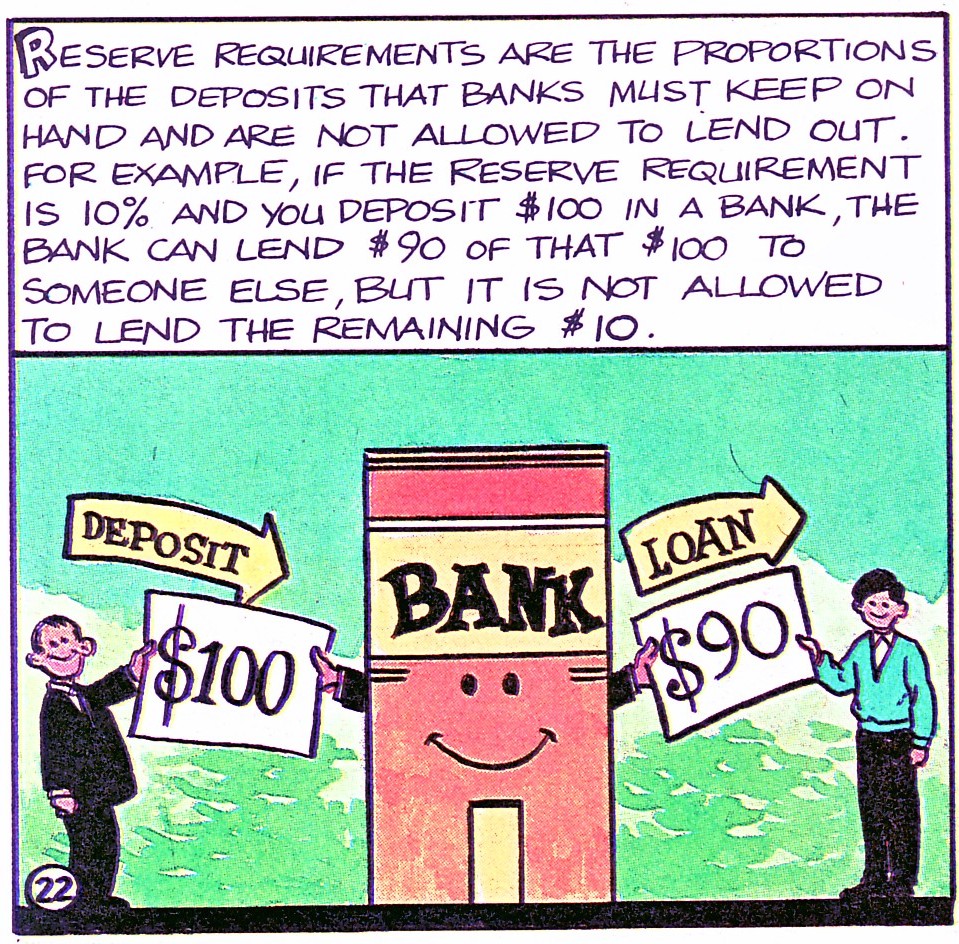

The Fed has a number of tools to influence the growth of money, and one is called “Reserve Requirements”. Reserve Requirements mean that a proportion of the deposits that banks receive have to be kept on hand. They are not allowed to lend it out. For example, if the reserve requirement is 10%, and someone deposits $100 in a bank, that bank can lend out $90, and they keep $10 on hand. That’s how banks make money. They take your money and lend it out to others in the form of automobile loans, mortgages, business, or personal loans, etc.

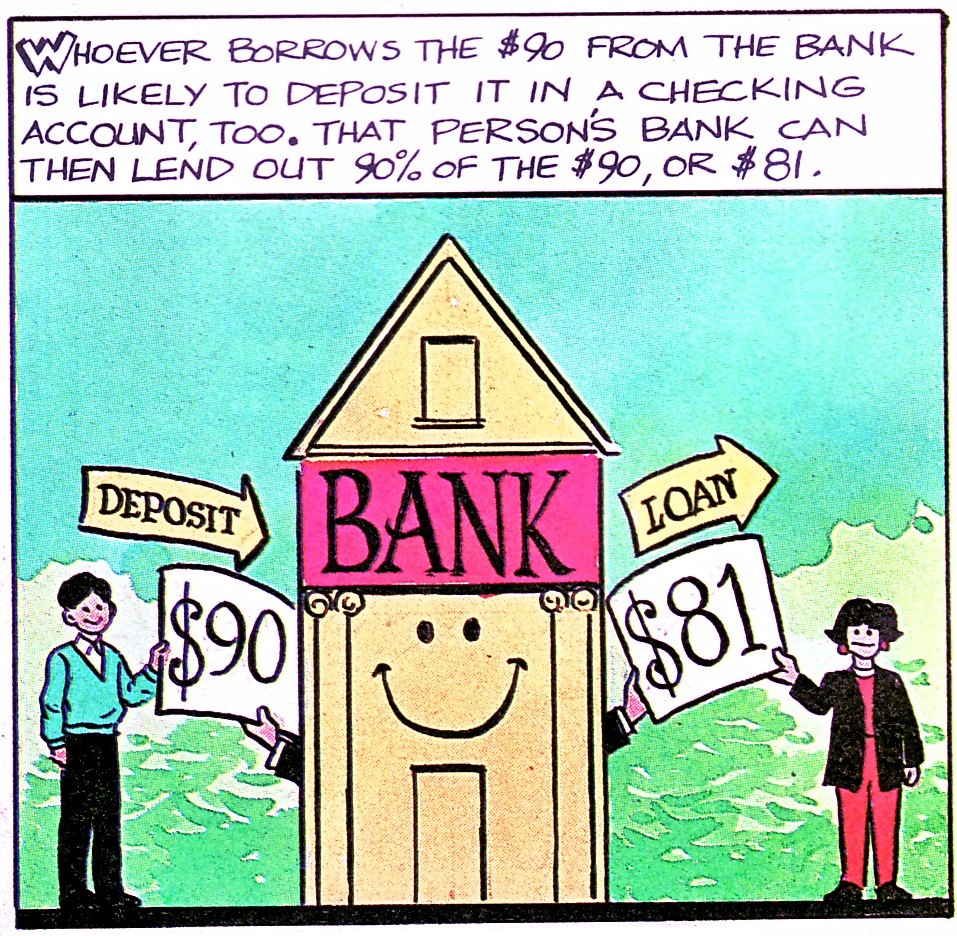

The borrower that just got $90.00 from your bank will likely deposit into their bank. Their bank can now lend out 90% of that $90.00, which is $81.00, and that bank is required to keep the other $9.00 on hand.

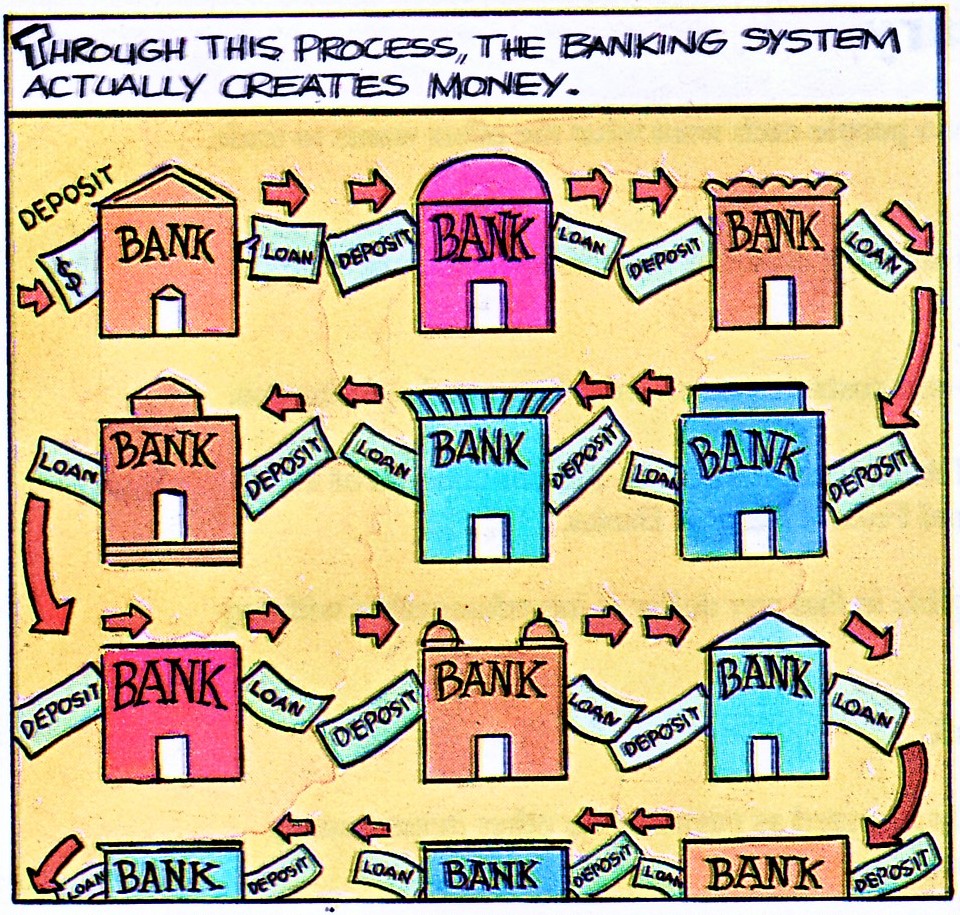

Through this process, the banking system actually creates money. Your deposit goes from one bank to another bank to another bank, and each of them has to hold onto 10% within their reserves, but the remaining can go out in the form of loans.

What is the actual current Reserve Requirement? According to www.federalregister.gov, as March 13th 2023, banks that are in between $15.2 million and $110.2 million in transaction accounts must hold 3% in reserves. Large banks, those who are in excess of $110.2 million in transaction accounts, must hold the reserve of 10%.

That’s probably where their problems started at the Silicon Valley Bank. Most of their loans were with businesses in the tech industry, and over the last 12-18 months, technology companies have had large decreases in business. So, this bank was probably not diversified enough in their business lending and all of a sudden found themselves coming up short when all of their borrowers were coming up short.

This is something that we don’t worry as much about here in the Midwest because we have a broad base of industries. At least those who had money at that bank, whether through the FDIC or from government intervention, will be able to get their deposits with no losses to individual taxpayers.

This explanation of the bank failure is my personal opinion. Other experts felt that the failure was caused by an over reliance on long term bond purchases that were at lower interest rates that had to be sold for a loss due to outgoing cash flows.

If you would like to have more information on how money works, and how it can work in your own individual economy, perhaps now is the time to schedule your Financialoscopy®.