Welcome to the Financialoscopy® Lab once again. Today, we are going to be talking about retirement planning. Specifically, we are going to be talking about income planning in retirement because at some point in time you’re going to want to say you’re done, you’re retired. Whether that is age 55, 60, 65, 70, or later, you need to have a stash of cash that you can live on for the rest of your life.

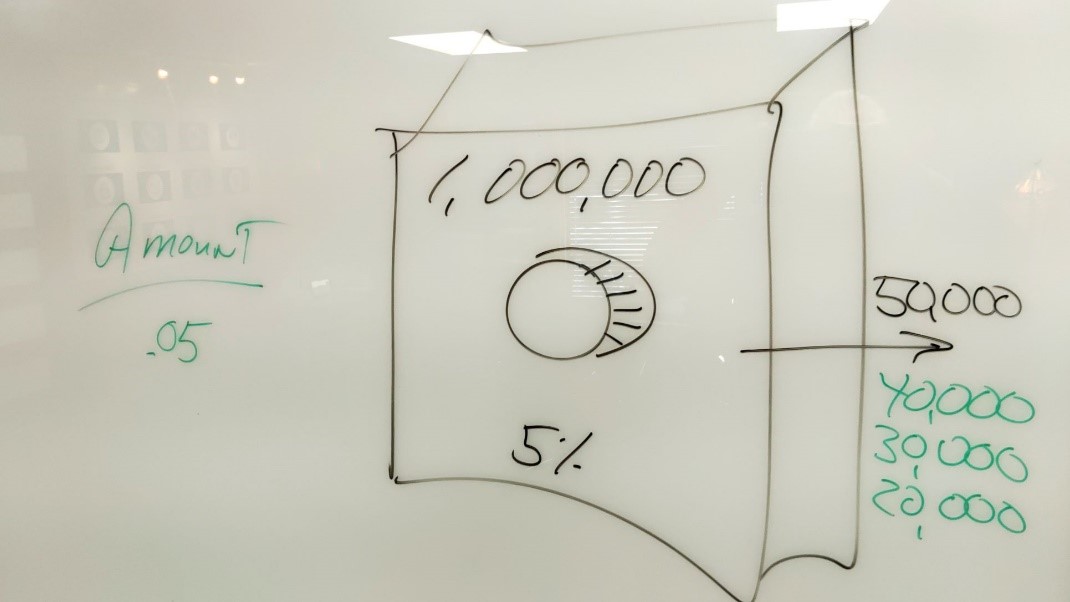

Let’s just say, in our example, that you are going to have $1,000,000. Now, you might be thinking, “Mark, I’ve got way over a million” or you might be saying, “Mark, a million dollars is but a dream”. The reason I’m using $1,000,000 today is because of the zeros. I want you to be able to go back to this video later on and do the simplistic math just based on the number 1 and a bunch of zeros. It’s going to be easier that way.

So, let’s say we have $1,000,000 and because we are older, we are probably dialing back the risk on the investments we’re making at the end of our lifetime. Because of that, I am drawing what appears to be a safe on our board so you can see that I’ve got my stash of cash. The reason I picked a 5% rate of return and wrote that at the bottom of our safe is because we’re really not looking for a 6-12% + rate of return anymore. We know with those types of returns we will have a lot of volatility. In fact, we might have volatility even at a 5% rate of return. The $1,000,000 is just a pretend number and the 5% rate of return is for illustrative purposes that I made up just to explain how this works.

So, you might believe that I am now a millionaire; I’ve got $1,000,000 dollars of stashed cash which is in my account. This $1,000,000, if I were to get a 5% annualized rate of return, might spin off $50,000 dollars in returns a year. This is the first ‘Ah-Hah’ moment. You are not a millionaire. You are a $50,000 dollars-a-year-aire. You can see how the 5% off of $1m provides $50k a year. The math works the same way with other numbers, a 4% rate of return would be $40k a year, a 3% rate of return would be $30k a year, 2% would be $20k, etc. I won’t go any lower. I don’t want anyone to be depressed, but you might be looking at Certificates of Deposit at a bank as a safe way to store stashed cash. However, at a bank, you may be hard-pressed to get much over 1% rates of return based on today’s date and what’s going on in the market.

The reason we can’t invest more aggressively is because if all of a sudden, the market goes down and you go from $1m to $750,000, where are you going to come up with $250,000 to replenish your stash of cash to bring you back up to the $1m to be able to distribute $50k on an annual basis? If you are thinking you don’t need $50k or maybe you’re thinking you need more, but let’s say you need less. Let’s say you have Social Security and a pension fund, or rentals and that has money coming in on a regular basis. How do you come up with your hard number in order to begin your retirement, even though that can be a moving target?

This is basically how you do that math:

- Take the amount of money that you believe you will need on an annual basis ($30,000)

- Divide that amount by the interest rate you believe you can reasonably get on an ongoing basis without fail. Again, we’re just going to pretend here because I want you to understand the math. This is not actually saying this is what you would receive. Let’s divide that amount by say 5%. That means you would divide the amount by .05 on a plain old calculator.

- $30,000 / 0.05 = $600,000

- So, I would need $600,000 to begin with at retirement to provide me with a 5% rate of return and my $30,000 a year.

This is what you need to remind yourself, a lot of people will say, “Mark, I never got a chance to touch the $1,000,000”. In essence, that is true to a certain extent because you are now self-insured. You are the one now who is always banking on you having this principle of $1m and having enough money to dole out what you need on an annual basis.

We also have to take into consideration this: not only are we taking out money on an annual basis, but every time inflation goes up, you will probably need to start taking out more and more and more. What happens over your lifetime is that because of the increases in the amount of money that you will need to take out, you will see your stash of cash decreasing over time. It is possible that at some point in time, in your old age, that it gets to zero ($0).

There are ways of combating this problem. We go through those options using actuarial science and the many other tools we have here at the Financialoscopy® Lab. We just want you to know that this is a simplistic way of looking at it. This may allow you to look at it very seriously or perhaps with a deer in the headlights look as you are looking at it now, but it’s better to look at this now as opposed to at retirement. This gives you a number that you need to reach in order to provide the income that you may wish to have in retirement.

If you would like to go through this math and much more complicated math based on your own life experiences, based on what you wish to accomplish, based on what you want to see for the whole of your life, it might be time to schedule your Financialoscopy®.